Solving For Retirement

Key Points:

The financial industry in Australia is grappling with the problem of turning accumulated savings into some kind of retirement income stream.

There is no silver bullet. The unique circumstances of every retiree means mass market, one-size-fits-all solutions generally fail to match investor preferences and needs.

We think the best solution to the retirement problem is good advice. The tools and portfolios available to advisers (including the ones we provide) give them the unique ability to generate retirement outcomes which align with investor needs.

How should Australia’s financial industry turn hard earned retirement savings into retirement income? Delivering investment outcomes in retirement is an incredibly complex problem, with any strategy having to solve for competing objectives, behavioural biases, personality differences and incredible uncertainties. At our core, we believe the best solution for retirement is good advice, it solves most of the above issues. Thankfully, our end investors are covered from that perspective. However, that still leaves a substantial proportion of the population looking for some kind of solution. The industry’s response to that problem is to create retirement products and portfolios, which makes sense. However, that leaves retirees little better off from a practical perspective. They still need to choose which solution works for them. Many of these solutions are very complex, even for sophisticated investment professionals. Most retirees have little hope. In this month’s Market Insight, we outline our thoughts on the issue.

Problems and Solutions

The only thing that is clear about retirement is that a one-size-fits-all approach is destined to fail. Every solution needs to trade off against competing objectives. These objectives differ person to person and may not necessarily be rational. Some retirees prioritise guaranteed income certainty, others want higher expected returns and the ability to leave a bequest. Some desire administrative simplicity (just spending portfolio income without selldowns for example), others are happy to actively manage their investments. Some are deeply conservative and worry about sequencing risk and drawdowns, some never bother to log into their accounts. Individual income needs can also change dramatically through retirement. The solution that worked at 65 may not be appropriate at 75. The challenge for the industry is that these deeply personal preferences cannot be captured in standardised products.

Below, we outline our thoughts on some of the readily available solutions.

Bucketing strategies solve for quite a few problems and have the ability to be highly customisable at the individual level. In decumulation, clearly having cash reserves is a requirement which a cash or liquidity bucket solves for. Theoretically, a mid-risk and growth bucket can be blended to balance the investor’s preference for income requirements and longevity as well. Bucketing strategies do a good job of combatting some of the behavioural biases in retirement, largely by framing each bucket in terms of easily understandable goals. However, where a bucketing strategy can fall short is in the portfolio construction phase. They can generate too much cash drag or move an investor outside their risk profile. Rebalancing between buckets can also be a challenge.

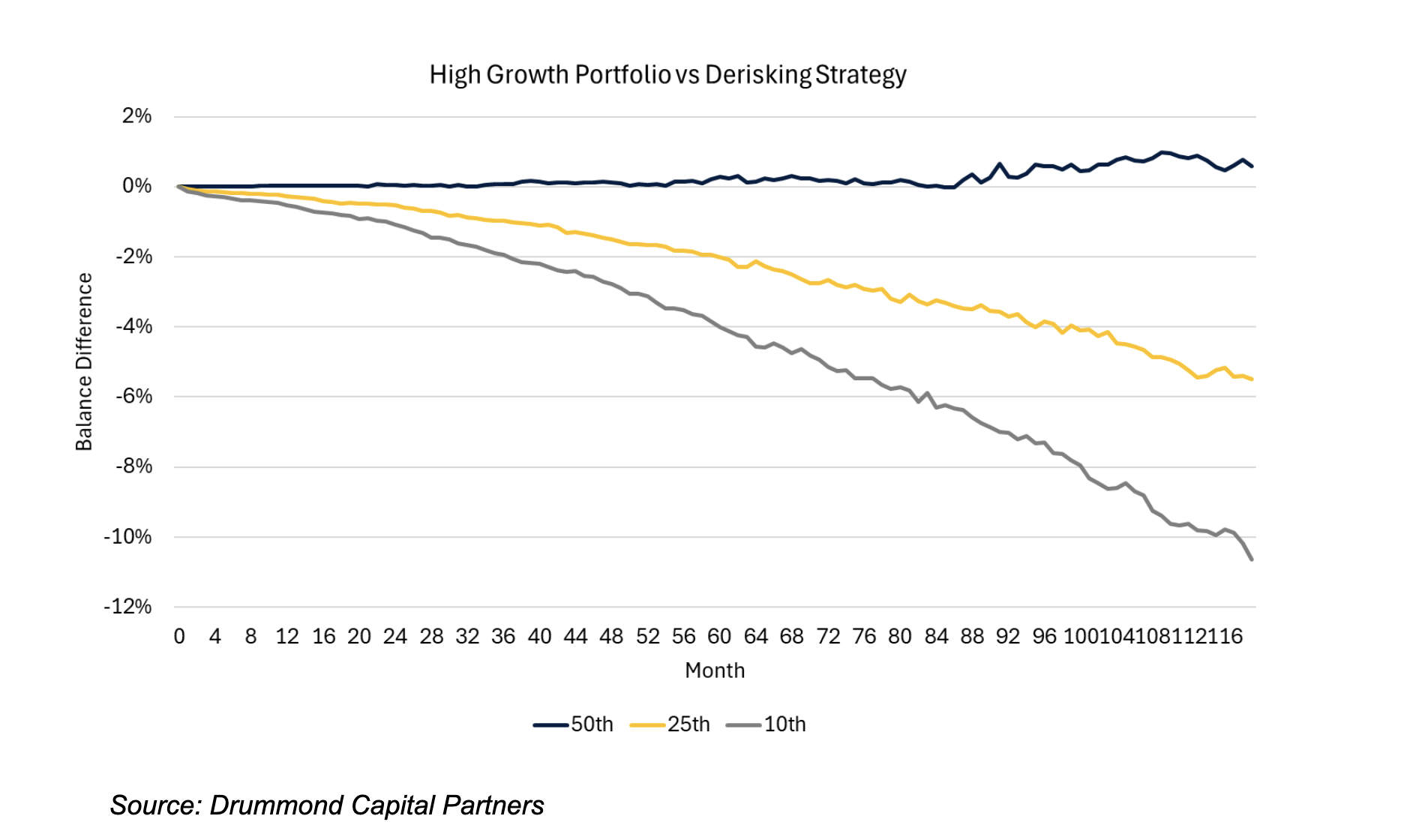

Target date and lifecycle funds are often the mass customisation solution of choice for default products. They are built on the principle that investor risk profile and / or investment requirements change as they approach and enter retirement. In practice, some combination of age and / or account balance is used to de-risk investors. Below, we show how they can work. In this simulation, a 90% growth portfolio is compared with a de-risking strategy that reduces growth exposure to 50% over a ten-year horizon. As expected, at the 50th percentile outcome, the 90% growth strategy outperforms. However, in negative investment environments the derisking strategy protects capital at a sensitive time in an investor’s journey. This has implications for lifetime retirement income as well. The difference between a $1,000,000 balance at retirement and a $940,000 balance (the difference between the 25th and 50th percentile outcomes is around $4000 per annum (in real terms) of growth portfolio income over a 30-year horizon. The de-risking can help provide income certainty.

Although they are popular, we think these strategies can be flawed. De-risking in these portfolios normally happens agnostic to the expected forward investment environment. A 55-year-old in 2010 may have spent five years selling very cheap equities and buying increasingly expensive bonds. By derisking in middle age, they can sacrifice too much longevity. It is often unclear whether that trade-off is a good one. Most people retire with decades of life ahead of them. How much to de-risk a portfolio is also extremely hard to do in an environment of unknown investor preferences. With that in mind, we think these strategies should be used cautiously.

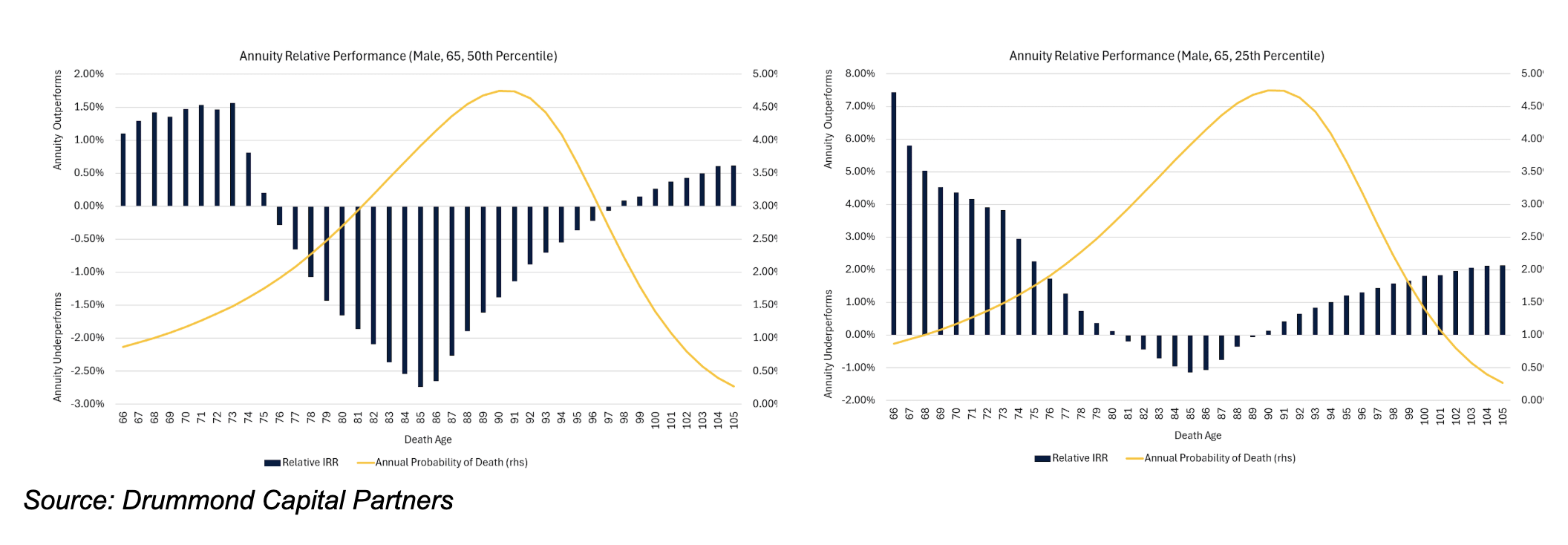

Longevity pooling / annuities offer perhaps the most direct solution to longevity risk, providing guaranteed income streams that can't be outlived, or some variation of the theme. Yet these products face significant behavioural hurdles—many retirees view them as unfair because those who die early subsidise those who live longer. The complexity of these products also makes them difficult for advisers to explain and clients to understand. Take the below charts for example. In these we compare at different death years the IRR of an inflation adjusted lifetime annuity (based on current payment rates) with the expected return from our DS 70 (growth) portfolio using our most recent capital market assumptions at two different percentiles. Not a very simple concept for a client to understand, let alone be able to make a decision about.

However, embracing the complexity, at the 50th percentile of growth portfolio returns, the annuity is overall not a good idea. It only outperforms the growth portfolio when the individual has a low probability of dying. The death probability (yellow line) weighted IRR differential is around 1% in favour of the growth portfolio. However, for many individuals, that 1% “cost” (plus all potential upside) is a small price to pay for certainty. Loss aversion is a common bias which is perfectly reasonable in retirement. The chart on the right shows that the annuity dominates the growth portfolio at the 25th percentile outcome. In other words, when markets are weak, the certainty of the income stream from the annuity plays its role. If a client needs absolute certainty in lifetime retirement income (or morbidly, if they are pretty sure they won’t make it to average life expectancy), a 1% return penalty from this annuity may be a reasonable price to pay.

Source: Drummond Capital Partners

Portfolios which blend some kind of annuity or insured income stream with market risk are also becoming widely available. They sometimes have the advantage of being able to generate regulatory arbitrage benefits (asset test discounts for age pensions for example). However, these products are very opaque, especially with respect to calculating the implied fee an investor is paying, and incredibly complex (they make annuities seem simple in comparison).

Tax-aware solutions represent another layer of complexity, particularly in Australia's unique environment of franking credits and superannuation tax concessions. These approaches focus on maximising after-tax income through strategies like franking credit optimisation, share buyback participation, and carefully managing the transition of accumulated gains into tax-advantaged pension phase accounts. However, this tax focus can sometimes prevent switching to better performing investment alternatives, creating a tension between tax efficiency and investment performance.

Income-focused portfolios are very common and aim to solve for both the strong psychological preference of investors to not sell assets and the practical problem of meeting cash requirements in retirement. While we think they have their place, too much focus on only income generation will often come at the cost of total return, which is something to be avoided, particularly in tax advantaged pension phase where there is no real tax cost to selling assets.

Doing nothing can also be a good strategy from an investment front. The best portfolio for an investor doesn’t necessarily change overnight because they were able to retire. Their risk profile may be unaffected by retirement, they may have sources of income outside their investment assets which meet their spending needs, they may have a multi-decade investment horizon.

Our Retirement Beliefs

We have a few foundational beliefs around how retirement portfolios and solutions should be built and delivered. In an ideal world, retirement solutions should aim to solve for maximum stable real income over expected retirement lifetime, incorporating both longevity protection and the flexibility to withdraw lump sum payments. This is difficult to achieve. Alongside this, we think solutions should be:

Dynamic and Forward-Looking: Active management is arguably more important in the years leading up to, and into retirement than during accumulation. Solutions should manage for sequencing risk and where portfolios are de-risked, those responsible should be highly aware of what the risks are in the asset classes they are being de-risked into. As 2022 shows, equity risk isn’t the only thing investors should worry about.

Structural Volatility Reduction: Volatility literally eats returns in retirement, particularly when regular withdrawals are required. Between two portfolios with similar expected returns, decumulators should always choose the one with lower volatility.

Risk Managed. Investors should carefully weigh tolerance for active risk against market risk. If capital can be preserved through a tactical investment process, then more structural market risk can be taken to enhance long-term returns.

Age Pension Integration: For individuals with very low superannuation balances, the age pension provides a substantial safety net that may justify taking more investment risk. Indeed, replacing the pension with a similar annuity would cost over $500,000 at current rates.

Stochastic Considerations: Individuals care far more about adverse outcomes (the 25th percentile) than about upside scenarios (the 75th percentile). This asymmetric concern requires portfolio construction and risk management approaches that prioritise downside protection over upside capture. Being aware of the “bad outcome” can also help give retirees the confidence they need to spend their assets and live a comfortable retirement.

Tax Awareness: Tax considerations (including franking) must be balanced against investment flexibility and performance considerations.

Where We Can Help

We believe that the best retirement solution is one that is advice led. That belief is relatively common across the institutional investor space. In line with this, we think our role in the process is to provide portfolios and tools which can help facilitate the best retirement outcome for individual clients.

Inflation is a key risk in retirement because investors lose their natural inflation hedge – their wage. A portfolio which has an inflation plus objective can provide good ballast in retirement, helping to re-establish some of that hedge. Portfolios which are designed to limit drawdowns and are managed to lower volatility are also particularly beneficial in retirement given the enhanced drag of volatility on returns in the decumulation phase. Income-focused portfolios can also play a role, particularly in bucketing strategies as a mid-risk allocation, assuming the total returns of the overall allocation are not sacrificed.

Ultimately, successful retirement outcomes aren't built from products alone. They emerge from the intersection of good advice, appropriate tools, and deep understanding of individual needs.

Prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, AFSL 534213. It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only. The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatements of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance. This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that it is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice.